The Social Security Crisis has become one of the most discussed financial concerns in the United States. Millions of Americans depend on Social Security benefits to support their retirement years, yet growing concerns about long-term funding continue to dominate public debate.

Experts, policymakers, and everyday workers are increasingly worried about what could happen if reforms are delayed.

For many families, the Social Security Crisis is not just a political issue. It directly affects retirement plans, monthly budgeting, healthcare decisions, and long-term financial security.

Rising inflation, longer life expectancy, and changing workforce trends are placing additional strain on a system that was designed decades ago for a very different economy.

At the same time, Americans are living longer than previous generations. While longer life expectancy is a positive development, it also means retirees are collecting benefits for more years.

Combined with declining worker-to-retiree ratios, this has intensified concerns surrounding the future stability of Social Security.

Americans Rethink Social Security Timing as Insolvency Fears Grow

The growing Social Security Crisis is changing how Americans think about retirement. Workers who once expected guaranteed benefits are now questioning when they should begin claiming Social Security and whether delaying retirement could provide greater financial security.

Financial advisors increasingly recommend that individuals carefully review their retirement timelines. Claiming benefits early may provide immediate income, but it can permanently reduce monthly payments.

Waiting longer often results in larger checks, but not everyone has the financial flexibility to delay retirement.

As the Social Security Crisis continues to dominate headlines, many Americans feel uncertain about the future. Younger workers worry that they may contribute to the system for decades without receiving the same level of benefits as current retirees.

Older Americans, meanwhile, fear potential reductions in monthly payments during retirement.

The emotional impact of this uncertainty is significant. Retirement decisions are no longer based solely on age or personal goals.

Instead, people are making choices based on concerns about inflation, healthcare expenses, and the long-term reliability of Social Security.

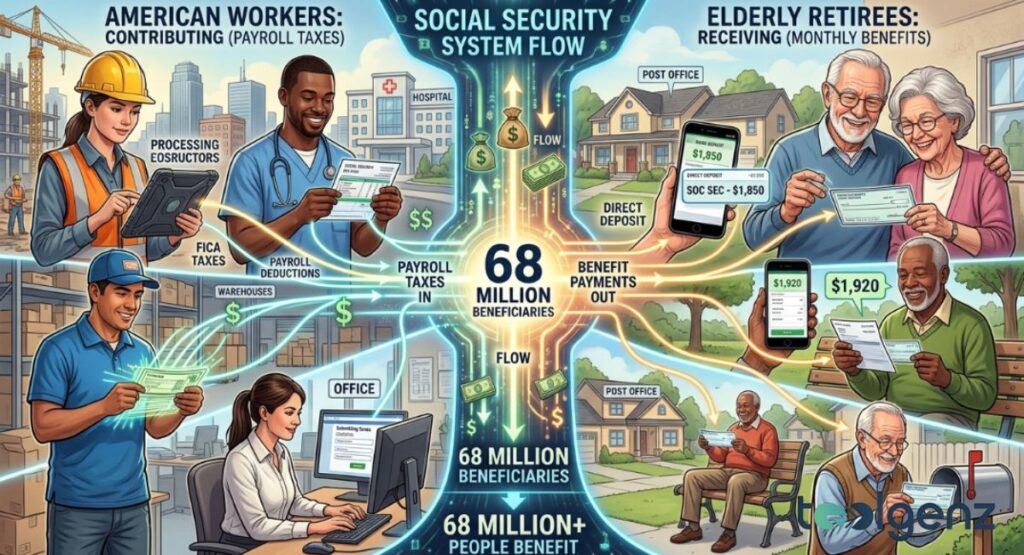

How Social Security Works and Why 68 Million Americans Depend on It

Payroll taxes from today’s workers fund benefits for 68 million retirees and disabled Americans.

To fully understand the Social Security Crisis, it is important to understand how the system works. Social Security operates primarily through payroll taxes collected from current workers.

Those taxes are then used to pay benefits to retirees, disabled individuals, and surviving family members.

Today, more than 68 million Americans rely on Social Security benefits. For many retirees, these payments represent the primary source of monthly income.

Without Social Security, millions of older Americans could struggle to afford housing, healthcare, food, and daily living expenses.

The Social Security Crisis has become more serious because demographic changes are reducing the number of workers supporting each retiree.

In previous decades, a larger workforce contributed taxes into the system. Now, declining birth rates and an aging population are placing greater pressure on available funds.

In addition, rising healthcare costs and inflation continue to increase financial stress for retirees.

Although cost-of-living adjustments help benefits keep pace with inflation, many seniors still feel that their monthly payments do not fully cover modern living expenses.

When Will Social Security Run Out? Key Timeline and Reserve Concerns

One of the biggest questions surrounding the Social Security Crisis is when the trust fund could become depleted.

According to several financial projections, reserve funds may face exhaustion sometime in the early 2030s if lawmakers fail to implement meaningful reforms.

This does not mean Social Security would disappear completely. Payroll taxes would continue flowing into the system, allowing partial benefits to be paid.

However, experts warn that future payments could be reduced if no long-term funding solution is introduced.

The uncertainty surrounding the Social Security Crisis has created growing anxiety among retirees and workers alike.

Many Americans are now paying closer attention to congressional debates and policy proposals related to Social Security reform.

Some analysts believe lawmakers will eventually act before major benefit reductions occur.

Others worry that political disagreements could delay meaningful action until financial pressure becomes unavoidable.

Fiscal Crisis Warning: The $193 Trillion Medicare and Social Security Shortfall

Long-term shortfalls for Medicare and Social Security now exceed $193 trillion.

The broader financial outlook connected to the Social Security Crisis extends beyond retirement benefits alone.

Analysts have also highlighted massive long-term obligations tied to Medicare and other government programs.

Combined projections for future liabilities have reached staggering levels, fueling concerns about federal spending and national debt.

Economists warn that if reforms are postponed for too long, younger generations could face higher taxes and reduced government flexibility.

The Social Security Crisis also raises important questions about intergenerational fairness.

Many younger Americans wonder whether they will receive the same benefits their parents and grandparents enjoyed.

At the same time, policymakers must balance competing priorities.

Protecting retirees is essential, but maintaining fiscal sustainability is equally important for the long-term health of the economy.

Cost-of-Living Adjustments (COLA) and How Benefits Are Updated

Inflation remains a major factor in the ongoing Social Security Crisis.

Social Security benefits are adjusted through cost-of-living increases, commonly known as COLA, to help retirees keep up with rising prices.

Although these adjustments provide some relief, many seniors argue that they do not fully reflect real-world expenses.

Healthcare, housing, and food costs often rise faster than official inflation measurements.

As the Social Security Crisis continues, lawmakers are discussing whether COLA calculations should be updated to better reflect the spending patterns of retirees.

Supporters believe this could help seniors maintain stronger purchasing power over time.

However, larger benefit increases could also place additional strain on the program’s finances.

This creates a difficult balancing act between protecting retirees and preserving long-term sustainability.

Market Futures and Economic Impact of Social Security Uncertainty

Benefit shortfall fears ripple through equities, bonds, and retirement risk indicators.

The economic effects of the Social Security Crisis extend far beyond retirement planning.

Financial markets, businesses, and consumers all react to uncertainty surrounding future benefits.

When people feel uncertain about retirement income, they often reduce spending and increase savings.

This can slow economic activity and affect industries such as housing, travel, and healthcare.

The Social Security Crisis also influences workforce behavior.

Many older Americans now choose to work longer than expected in order to strengthen their financial position before retirement.

Economists continue studying how retirement uncertainty affects investment decisions, consumer confidence, and long-term economic growth across the country.

Options to Extend Social Security Solvency and Avoid Collapse

Addressing the Social Security Crisis will likely require a combination of reforms rather than a single solution.

Policymakers have proposed multiple strategies to strengthen the system and improve long-term solvency.

Some proposals focus on raising payroll taxes for higher earners, while others recommend adjusting future benefit formulas.

Certain experts support gradually increasing the retirement age to reflect longer life expectancy.

The debate over the Social Security Crisis remains highly political because every proposed solution affects different groups in different ways.

Some reforms could reduce future benefits, while others may increase tax burdens on workers.

Despite disagreements, many experts agree that delaying action could make future reforms more painful and expensive.

Policy Reforms: Benefit Caps, Inflation Indexing, and Retirement Age Changes

Congress weighs benefit caps, inflation formulas, and raising the retirement age to 68.

Several reform proposals connected to the Social Security Crisis focus on modifying how benefits are calculated.

One common idea involves adjusting benefit caps for higher-income retirees.

Other proposals recommend changing inflation indexing formulas to slow the growth of future payments.

Supporters argue that these changes could help preserve the program without imposing dramatic cuts.

The Social Security Crisis has also intensified debate about raising the retirement age.

Advocates believe Americans are living longer and healthier lives, making gradual increases reasonable.

Critics, however, argue that raising the retirement age could disproportionately affect lower-income workers and individuals in physically demanding jobs.

Beyond Social Security: Smart Ways Americans Can Save for Retirement

Because of the uncertainty surrounding the Social Security Crisis, financial experts encourage Americans to build additional retirement savings outside government programs.

Popular retirement tools include 401(k) plans, IRAs, personal investments, and diversified savings portfolios.

These options can provide additional financial protection during retirement.

The Social Security Crisis has encouraged many younger workers to become more proactive about long-term financial planning.

Rather than depending entirely on government benefits, individuals are increasingly seeking independent sources of retirement income.

Financial literacy also plays a critical role in retirement preparation.

Understanding budgeting, investing, and risk management can help families make more informed decisions about their future.

The Bigger Picture: Deteriorating Fiscal Space and Long-Term Reform Challenges

Rising debt, interest rates, and deficits shrink options for entitlement reform.

The long-term challenges connected to the Social Security Crisis reflect broader economic and demographic trends across the United States.

An aging population, rising healthcare costs, and growing national debt all contribute to increasing financial pressure.

Many experts believe these long-term financial challenges cannot be solved through temporary political compromises alone.

Instead, sustainable reform may require difficult decisions involving taxes, benefits, retirement age policies, and long-term government spending priorities.

Despite these concerns, Social Security remains one of the most important programs in American history.

Millions of retirees depend on it for stability and financial security.

The future of the system will ultimately depend on how quickly lawmakers act and whether bipartisan solutions can be achieved before funding pressures become more severe.

FAQs

Is Social Security at risk of insolvency?

Yes. Financial projections suggest that reserve funds could face depletion in the early 2030s if reforms are not implemented.

What are the three ways you can lose your Social Security?

Benefits may be reduced through policy changes, delayed retirement eligibility, or lower payouts caused by funding shortages.

What changes are coming to Social Security for 2026?

Most expected changes involve annual cost-of-living adjustments designed to help benefits keep pace with inflation.

What will happen to Social Security in 2033?

If no reforms are passed, future benefits could be reduced because incoming payroll taxes may not fully cover scheduled payments.

How close are we to losing Social Security?

Social Security is not expected to disappear entirely, but funding challenges may affect full benefit payments within the next decade.